View: Stocks are cash makers now but be knowledgeable that some buyers continue to haven’t recovered from the 2000 internet bubble

Table of Contents

How many years of lagging stock portfolio returns would you tolerate in purchase to avoid the bursting of a stock marketplace bubble?

That in influence is what Wall Street’s “permabears” are asking. They’ve been bearish on U.S. stocks for a variety of years now, and therefore they (and their clientele) have skipped out on just one of the most powerful bull markets in U.S. heritage.

Jeremy Grantham is a single of the most prominent permabear he is co-founder of Grantham, Mayo, & van Otterloo, a Boston-primarily based asset management company that is commonly recognised by the acronym GMO. Grantham has a amount of remarkable current market phone calls to his credit score, such as mainly sidestepping the bursting of both of those the online bubble and the Wonderful Recession. But he is not generally bearish. In March 2009, the thirty day period in which the Wonderful Economical Crisis-induced bear sector came to an end, Grantham amazed a lot of on Wall Street by penning a letter imploring supervisors to develop a approach for acquiring back again into stocks.

Yet in most fiscal circles, in which a “what have you done for me lately” frame of mind prevails, Grantham is recognised for failing to foresee the previous decade’s bull market place. Back again in 2010, scarcely a 12 months immediately after the U.S. bull market commenced in March 2009, GMO projected that U.S. big-cap shares would hardly outperform inflation around the subsequent 7 yrs.

As we now know, of class, U.S. shares in modern years have been beating inflation by historic margins. Since 2010, the S&P 500’s

SPX,

inflation-modified total return has been 12.5% annualized.

GMO’s response, in outcome, is that caution could be vindicated and it would get the past giggle. In a new examination entitled “Wounds That Under no circumstances Mend,” GMO argues that all it would just take would be anything equivalent to the bursting of the world-wide-web bubble in March 2000 or the bear market that accompanied the stagflation period of the 1970s.

Given that this reaction is self-serving on GMO’s element, I determined to independently evaluate the prolonged-time period affect of residing by the bursting of a bubble. What I found is sobering without a doubt. There have been occasions in U.S. stock sector history—not as rare as we would like — when unlucky buyers lost so considerably that it took a technology or additional to recuperate.

If Grantham is proper that the recent inventory market is forming a bubble that is about to burst, he’s also right that “for the majority of traders right now, this could very well be the most crucial celebration of your investing lives.”

The 6% remedy

Just one way of measuring the lingering effect of a bubble bursting is to estimate how extensive it usually takes for the inventory marketplace to make it back to its extended-expression craze line. Due to the fact 1793, according to investigation from Edward McQuarrie, an emeritus professor at Santa Clara University’s Leavey College of Business enterprise, the U.S. inventory marketplace has developed an inflation-modified full return of 6.05% annualized. For illustration reasons, I’ll spherical that to 6 percent.

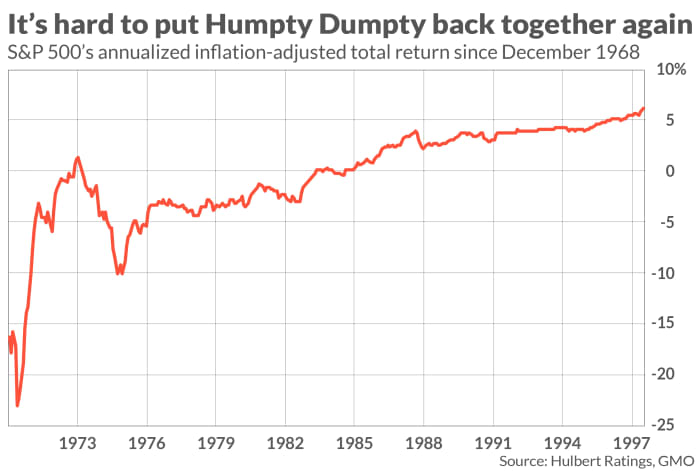

Visualize an trader in December 1968 to assemble a portfolio that would fiscally assistance his retirement. His money planner nearly absolutely would have turned to record to determine this portfolio’s anticipated return, and so would have projected that — 12 months-to-calendar year volatility aside — the equity portion of his portfolio would produce a 6% annualized actual complete return around the subsequent decades.

I picked December 1968 to illustrate my position, as that marked a generational higher. The chart under plots this investor’s annualized inflation-modified overall return from that month forward. You can see the devastation wrought by the 1973-74 bear market, as nicely as the significant-inflation a long time of the 1970s and early 1980s. But, most of all, detect that it’s not till mid-1997 that this investor’s extended-term return would make it back to 6% annualized. That is practically 30 yrs.

You could speculate why I didn’t target on the bursting of the web bubble in March 2000. The remedy is that an investor unfortunate sufficient to put a lump sum into the marketplace at that time continue to has not sufficiently recovered from losses so as to make it again to the 6% trendline. That investor’s serious complete-return because that day is 5.1% annualized. So 21 many years have not been enough to vindicate the investor in March 2000 who primarily based his fiscal long run on extrapolating the very long-phrase previous.

Who believes in 6% any more?

You also could object to the sobering message of my evaluation on the grounds that no one expects the stock market to generate a extensive-time period authentic whole return of 6% annualized. In the low-curiosity-rate low-development planet in which we now are living, you could argue, it is unrealistic to assume the inventory market’s foreseeable future return to be as extraordinary as in the past.

Old beliefs die hard, however. You’d be surprised to master that several economical planners proceed to build financial strategies for their customers on the assumption (implicit if not express) that the long term is like the previous. It is also the implicit assumption behind the glide paths adopted by quite a few of the concentrate on-date retirement funds that are so well-liked for 401(k) buyers and retirees.

Nevertheless, your objection is not unfair. So it’s also worth focusing on how lengthy traders will need to simply crack even next the bursting of a bubble.

Fortuitously, the significant lifting of such calculations has been executed by McQuarrie. For the period relationship again to 1793, he calculated the longest stretch in which the inventory market’s inflation-adjusted total return was much less than 1% annualized. The longest was the time period starting with the 1929 crash: From then right until 1949, the inventory sector developed an inflation-altered total return of .75% annualized — 20 years, in other words.

Which is much better than the practically 30 years it took immediately after an unfortunate investor in December 1968 to make it back to the 6% trendline, but not by substantially.

Bubble difficulty?

None of this sheds light on no matter whether we are in a bubble, of system. All this discussion does is show that getting careful for a 10 years is not automatic grounds for concluding that the adviser has unsuccessful his clientele.

The arguments for why the stock current market is exceptionally overvalued, if not in a bubble, are acquainted, and I will not repeat them below. But supplied Grantham’s history at detecting prior bubbles, and provided the extensive-time period hurt a bubble bursting would have on our portfolios, I would be anxious dismissing his warning out of hand.

Mark Hulbert is a frequent contributor to MarketWatch. His Hulbert Scores tracks financial commitment newsletters that pay back a flat charge to be audited. He can be reached at [email protected]

Much more: Harvard’s endowment return is even worse than the S&P 500 and that must be a lesson for your possess portfolio

Plus: At the rear of best U.S. inflation fee in 31 many years lurks panic that Federal Reserve has `lost control’ of consumer prices