Prosus Stock: New Artificial Intelligence Capabilities, And Cheap (OTCMKTS:PROSF)

")

Table of Contents

Kativ/E+ via Getty Images

Prosus (OTCPK:PROSF) reports a significant amount of cash in hand to acquire new targets. The company is using artificial intelligence capabilities to offer more personalized recommendations to users. Besides, PROSF’s food delivery is increasing its offering by delivering groceries. With double-digit revenue growth and growing free cash flow, PROSF’s DCF model results in a valuation of $155 per share. In my view, the current market price is a joke, and I will be buying shares.

Prosus Invests In Growing Markets And Is A Skilled M&A Player

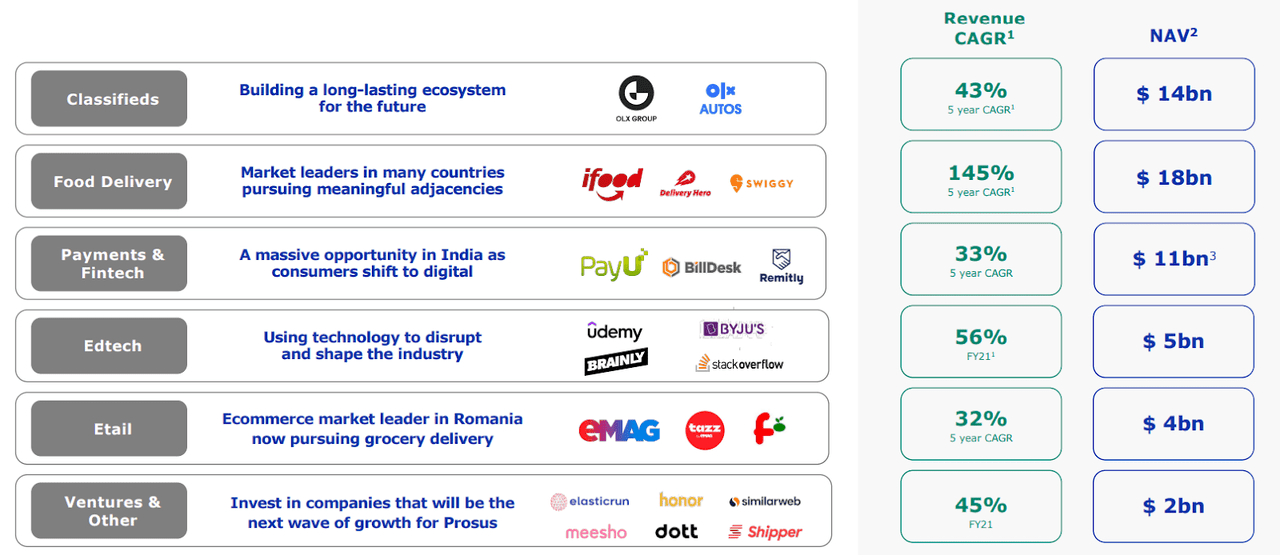

Prosus is a holding that is investing in high-growth markets like online food delivery, fintech, and classifieds. Management finds target markets that are growing at a double-digit rate. Most of the business segments operated by Prosus report sales growth between 32% and 145%:

I believe that most analysts will be expecting significant revenue growth in the coming years. Note that the company has reported 53% sales growth y/y, and management is targeting an internal rate of return close to 22%.

I cannot really say whether Prosus will deliver the same results in the coming years. However, I believe that it is quite likely that sales growth continues at a double-digit rate. This is also the belief of many investment analysts.

Source: IR

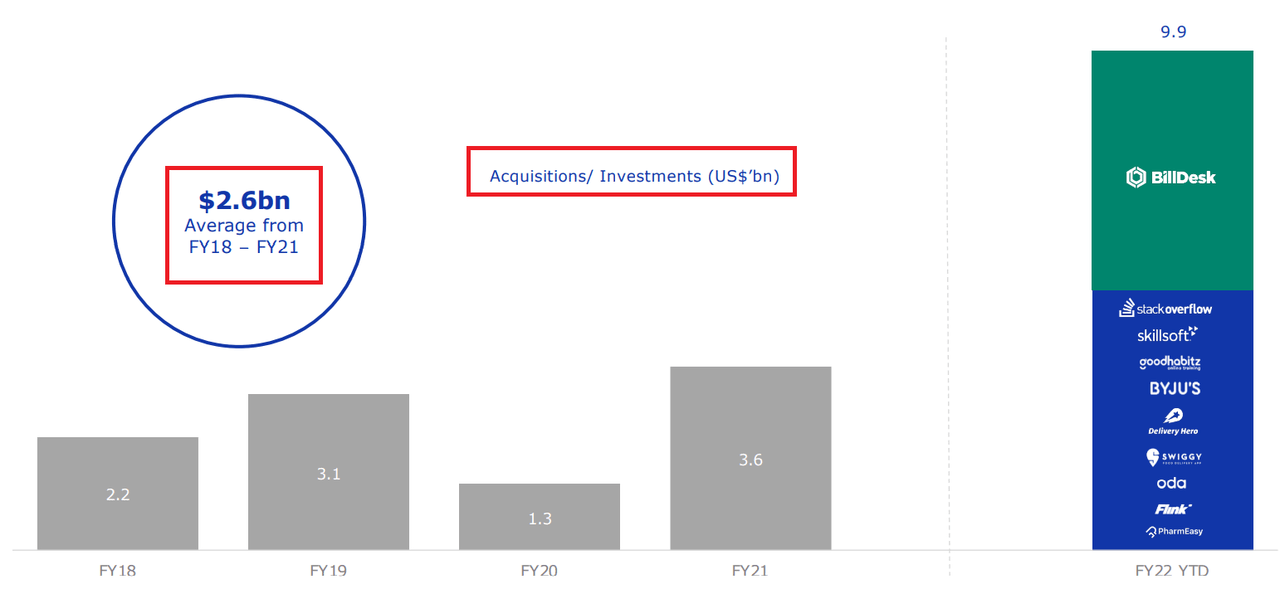

I am also quite optimistic about the future transaction executed by Prosus. Note that the company makes on average close to $2.6 billion via acquisitions and investments. Given the increase in the net asset value of the portfolio, I believe that management is quite skilled in the M&A market. It knows how to identify growth as well as to sell companies at a decent multiple. In the future, I would expect this know-how to enhance the portfolio growth:

Source: IR

Balance Sheet: Cash In Hand For New Acquisitions, And Goodwill

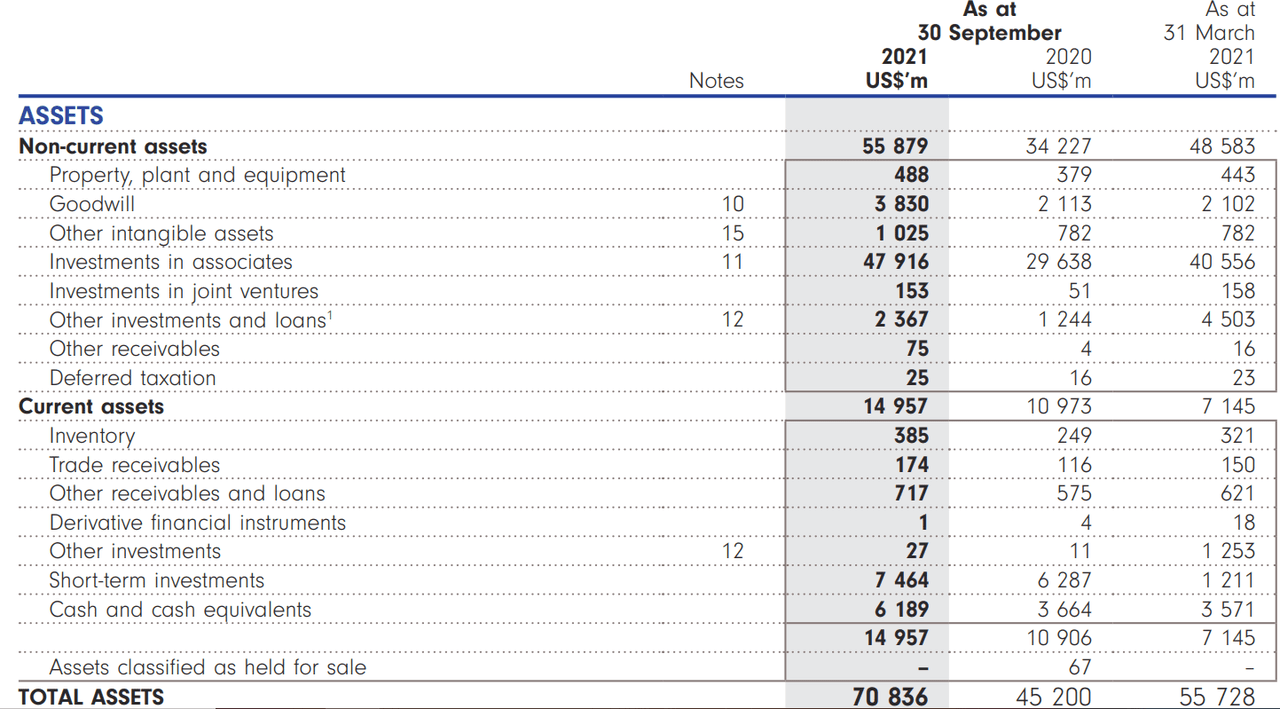

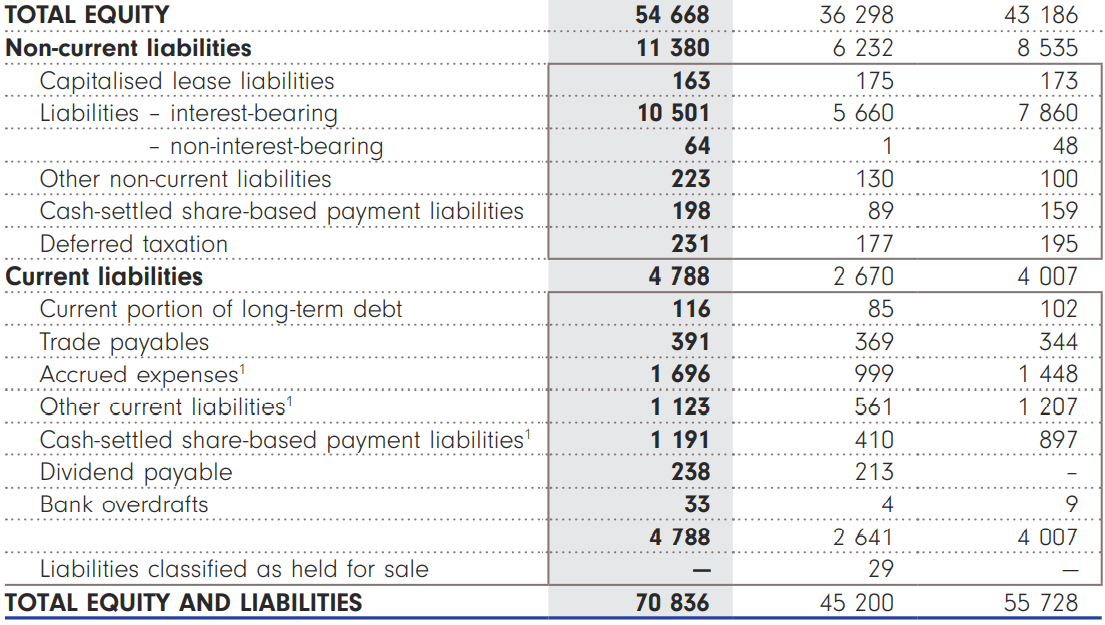

As of September 30, 2021, Prosus reported $6 billion in cash and $7 billion in short-term investments. I believe that the company has sufficient liquidity and financial shape to acquire new targets or make new investments.

Management also reported $3.8 billion in goodwill, which I appreciate for two reasons. First, it means that management has expertise in the acquisition of targets. We could expect more acquisitions in the future. Second, if management has successfully calculated the operating synergies, we could be expecting revenue and FCF growth.

I am not concerned about the current amount of leverage. The company reports financial debt of close to $10.5 billion, but the net debt is negative:

Source: Quarterly Report

Base Case Scenario With Artificial Intelligence And Online Grocery

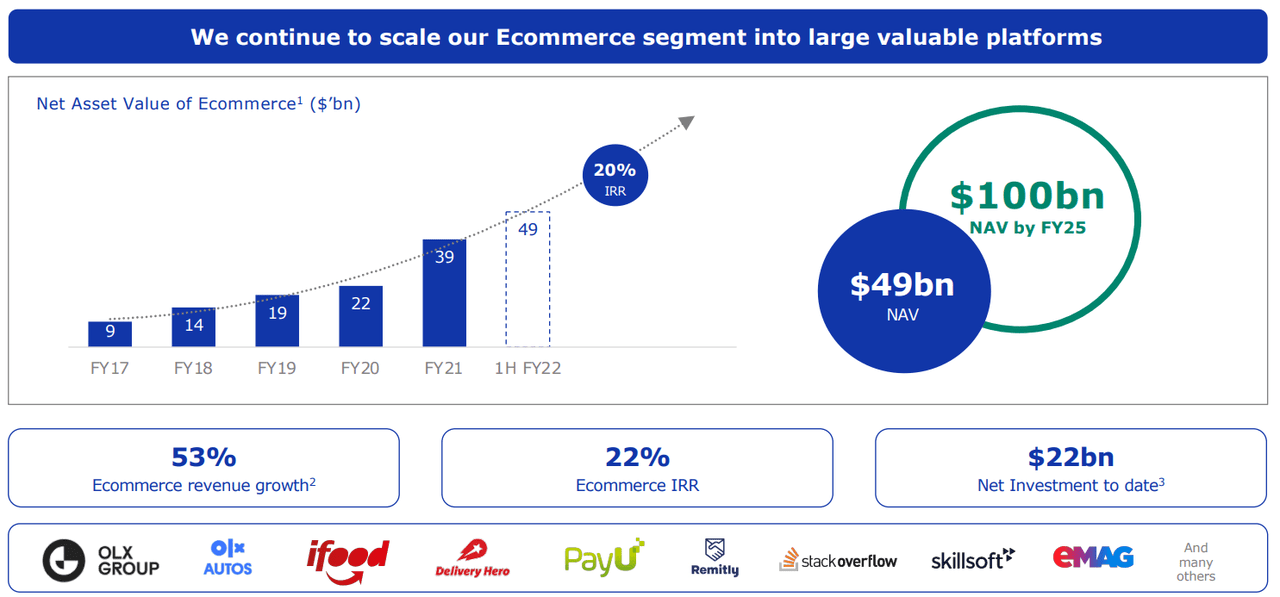

I believe that Prosus will make tons of money once the company’s food delivery business segment increases its offering. If the company is successful in bringing groceries to clients, the target market will most likely significantly increase:

Online grocery presents a large growth opportunity, where structural category dynamics are attractive (high frequency and average order value) but online penetration is low compared to other ecommerce categories. We have seen a significant switch over the past year, with the market’s transition to online accelerated by the pandemic.

We will continue to grow our core food-delivery markets and build adjacencies – local food-service brands, grocery and convenience delivery, and more. Source: Annual Report

Regarding the company’s classifieds business segment, I am quite optimistic about the new artificial intelligence training offered by Prosus. Management noted in the annual report that the company’s machine learning capabilities enhanced personalized recommendations to users. In my opinion, if investments in AI technology continue, and it is also used in other companies owned by Prosus, revenue growth could be substantial:

During the year, our ML models had a substantial impact on our search, lead qualification, and trust and safety initiatives. This has enabled us to advance further in becoming a smart, convenient and trusted way for people to make big and small life choices. Personalised recommendations using item2vec technology enable our products to make ‘smart’ alternative suggestions to our users. Accurate job recommendations, as well as online price valuation in the motors category, are prime examples of offering transparency and peace of mind to our customers. Finally, automated content moderation keeps our platforms safe and trusted. Source: Annual Report

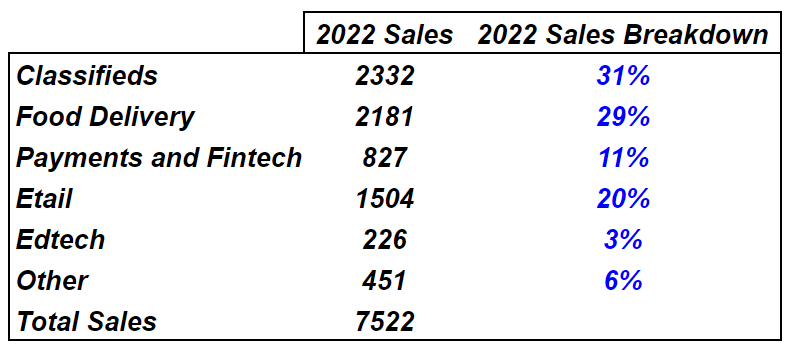

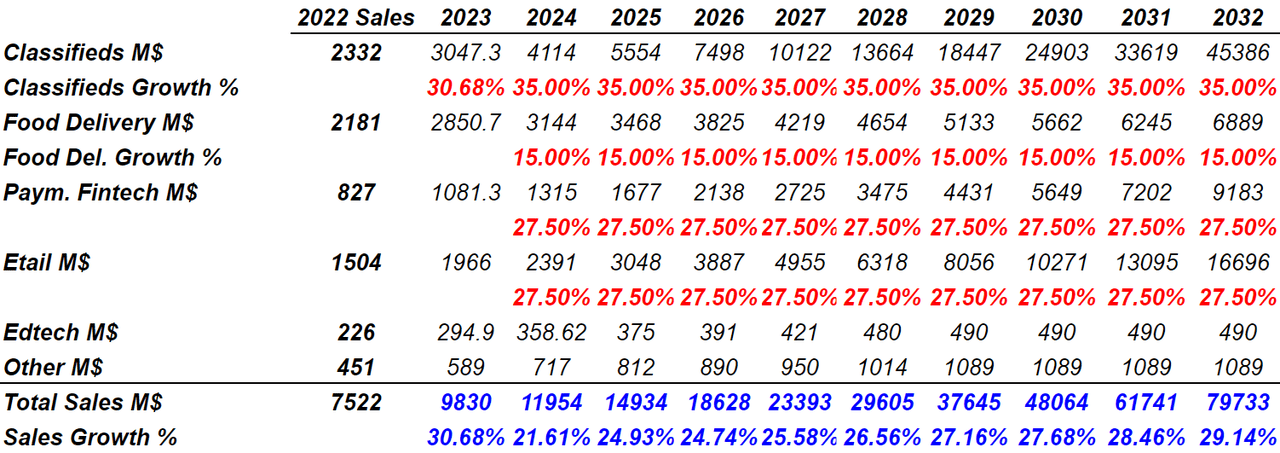

I made several assumptions about the future revenue breakdown. In 2022, I believe that the most relevant business segments will be online classifieds with 31% of total revenue, food delivery with 29% of the total amount of sales, payments, and fintech. I will also assume 2022 sales of $7.5 billion:

My Figures

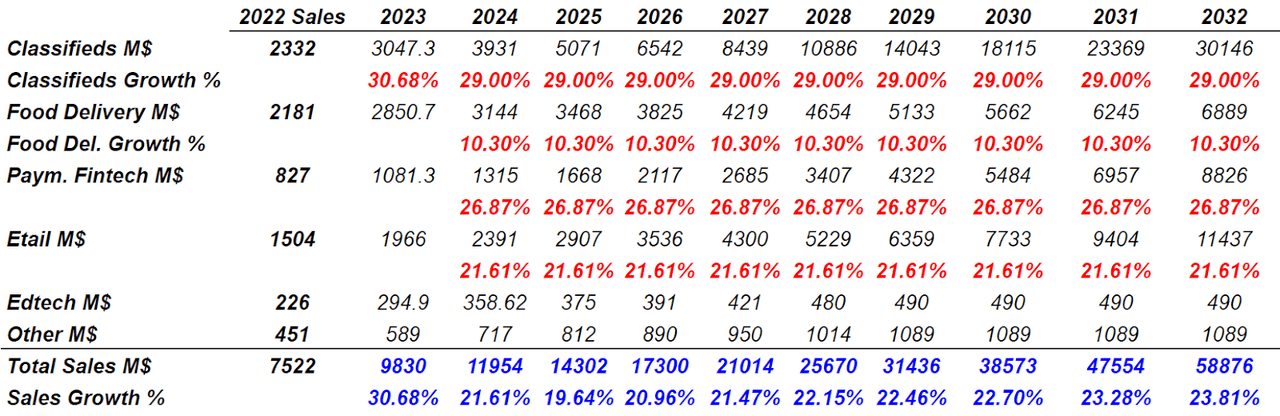

I studied the growth of each target market to design my first DCF model. I assumed that the classifieds business segment will grow at a CAGR of 29% because the e-commerce market is expected to grow at that rate:

Global E-Commerce Market 2021-2025 The analyst has been monitoring the e-commerce market and it is poised to grow by $ 10. 87 trillion during 2021-2025, progressing at a CAGR of almost 29% during the forecast period. Source: The Global E-Commerce Market

I also assumed that the food delivery would grow at a CAGR of 10%, and the fintech’s growth would stay close to 27.5%:

The global online food delivery services market size is expected to grow from $115.07 billion in 2020 to $126.91 billion in 2021 at a compound annual growth rate (CAGR) of 10.3%. Source: Online Food Delivery Services Market Growth To Accelerate

The “Global FinTech Market, By Technology, By Service, By Application, By Region, Competition Forecast & Opportunities, 2026” report has been added to ResearchAndMarkets.com’s offering. The Global FinTech Market was valued at USD7301.78 billion in 2020 and is projected to grow at a CAGR of 26.87% during the forecast period. Source: Global FinTech Market Report 2021: Market was Valued at (globenewswire.com)

My results include 2032 sales of close to $58.85 billion, and FCF margin of close to 23%. I believe that my figures are close to the expectations of other analysts out there:

My Figures

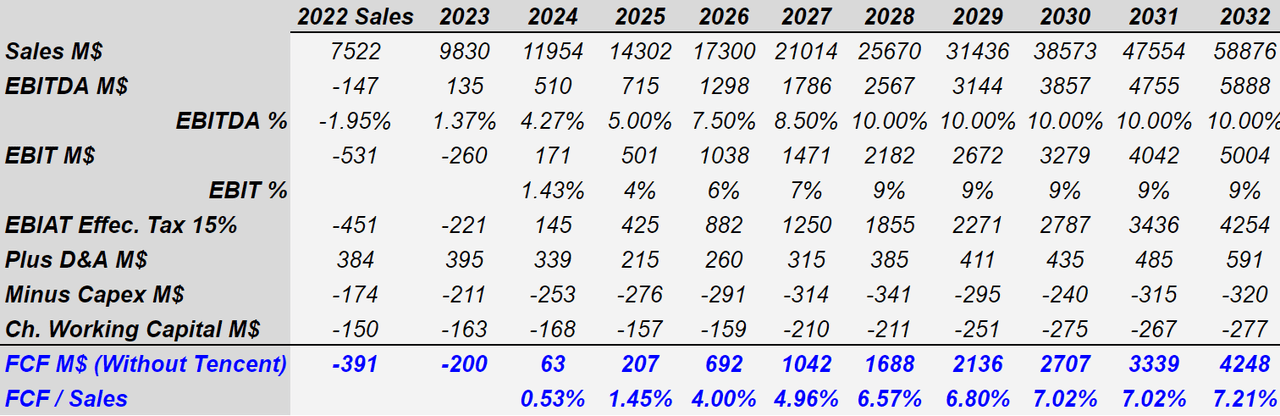

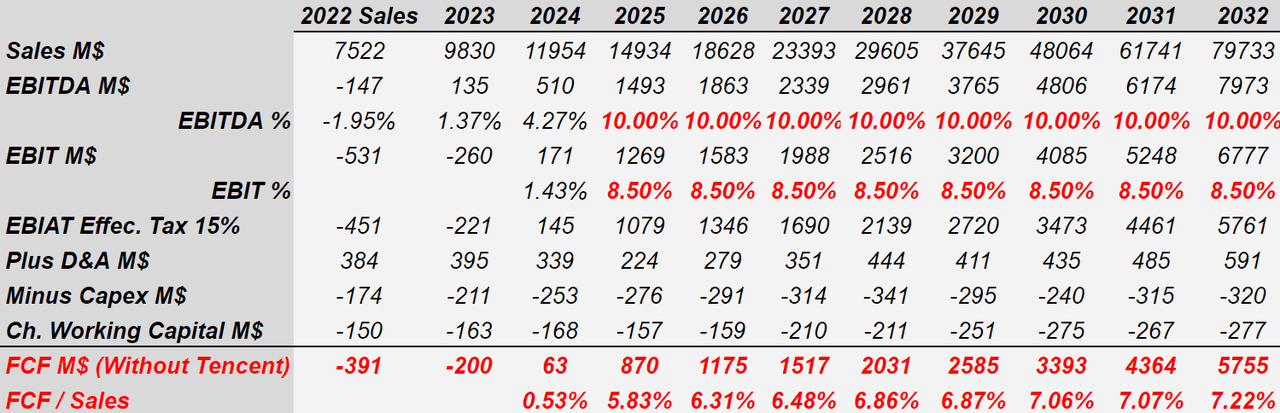

Using the previous sales figures, I assumed an EBITDA margin of 5%-10%, which I believe is conservative in the tech sectors in which Prosus invests. I also added depreciation and amortization of $350-$600 million, and capital expenditures worth $200-$320 million. Finally, the resulting FCF/Sales would stand at 0.5%-7.5%, and 2032 FCF would stay close to $4.25 billion:

My Figures

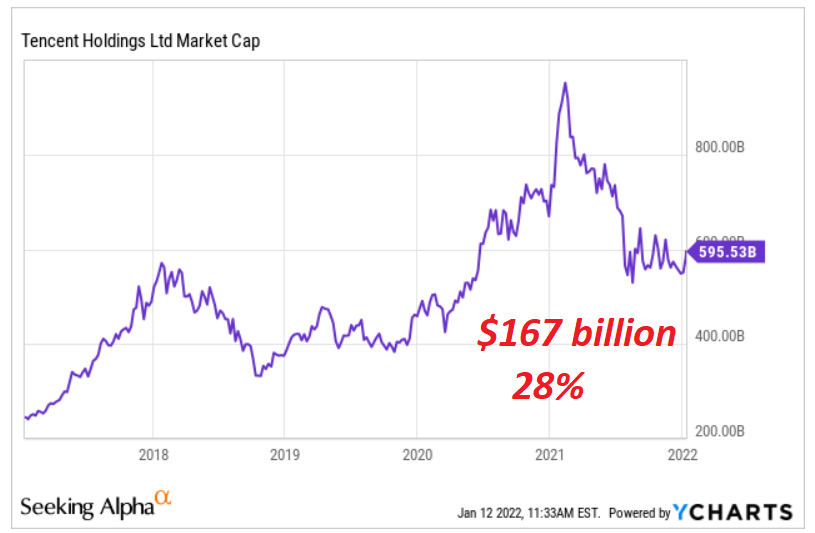

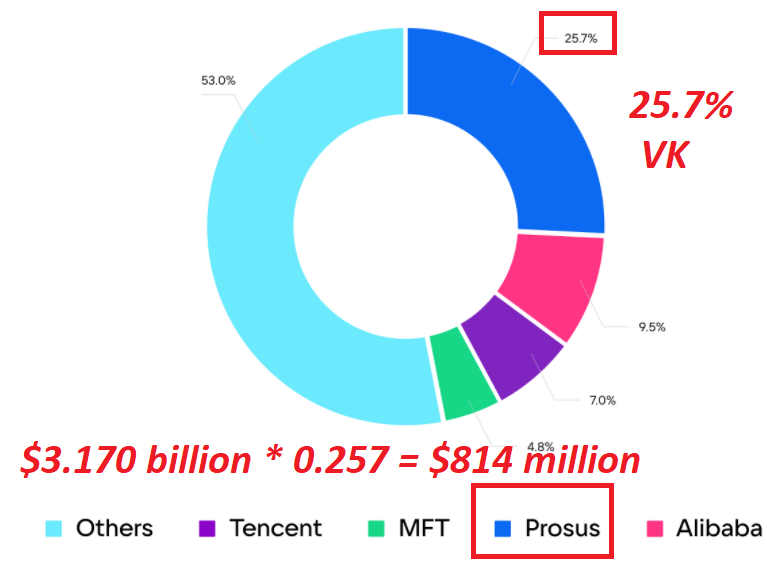

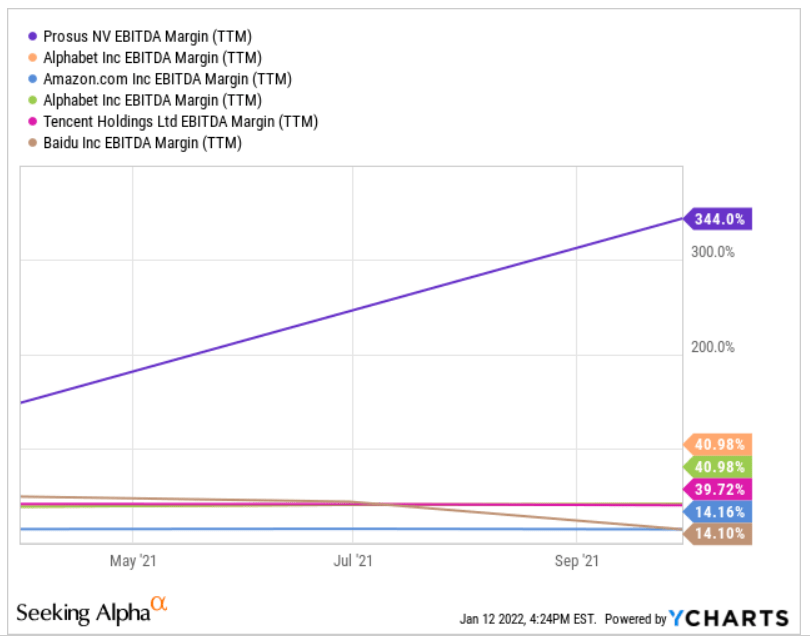

In this case, including some of the associates in which Prosus invested is very relevant. The company owns 28% of Tencent (OTCPK:TCEHY), and 25.7% of VK (OTC:MLRYY). In total, I believe that these two investments are worth $167.814 billion:

Ycharts

I took a look at some of the competitors and their EV/EBITDA multiples. Peers trade at 10x-41x FCF. However, I believe that Prosus could trade at much more than its peers because it holds investments in companies that are very young. Their business history will most likely be longer than that of competitors, so using a large EV/FCF makes sense:

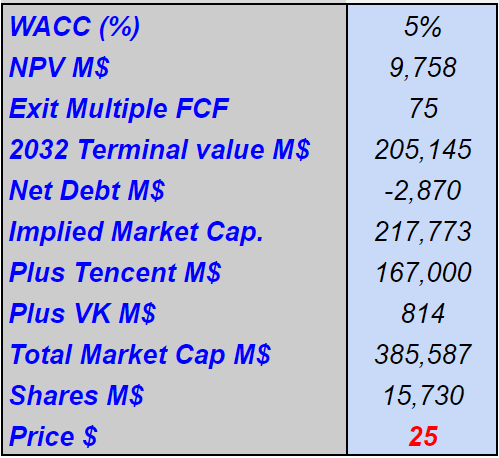

Putting everything together, I used a WACC of 5%, which implied a 2032 terminal value of $205 billion, and a net present value of $9.75 billion. If we sum the stakes in Tencent and VK and divide by 15 billion shares, the target price stands at $25:

Source: My Results

Best Case Scenario Would Include Brilliant Acquisitions And Intensive M&A Operations

In the best-case scenario, I will be assuming that Prosus will buy and invest in impressively profitable companies. Notice that Prosus usually targets an internal rate of return of 20% for early-stage partnerships. So, in this case, I would be expecting many of such successful deals:

For early-stage partnerships in new or high-growth markets, the risk profile is clearly high. In these cases, we look for venture-style IRRs well over 20%, understanding that operational success will determine the outcome. Source: Annual Report

I would also expect mergers among the company’s owned by Prosus. Think about it. Prosus has many companies operating in the same business segment. In my view, if management decides to merge some teams, shareholders may benefit from certain operating synergies. As a result, we could see an increase in the FCF margins:

I would also include an increase in the company’s net income thanks to transactions, sales, and other disposals. The company sells and buys companies on a daily basis. I am not thinking out of the box by assuming that more transaction could be very beneficial for Prosus. In this regard, let me mention one example of a transaction executed by Prosus. It is the merger between OLX and OfferUp, which resulted in a net gain of $114.8 million.

In July 2020, OLX merged its US letgo business with OfferUp, two of America’s most popular apps to buy and sell in the US. OLX contributed its US letgo business. The total consideration was US$360.0m, including cash of US$100.0m. On disposal of the US letgo business, the group recognised a gain of US$114.8m in ‘Net gains on acquisitions and disposals’. Source: Annual Report

Under this particular and a bit unlikely case scenario, I assumed that the classifieds business segment would grow at 35% y/y. I also believe that with sufficient M&A transactions, food delivery sales could reach 15% sales growth, and the fintech sales growth could reach 27.5%. In sum, 2032 sales would be equal to $75-$85 billion:

My Figures

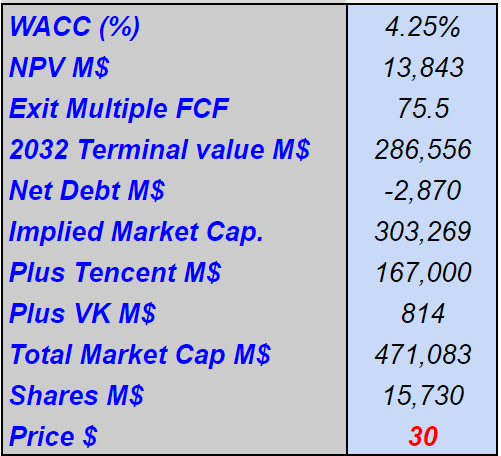

I assumed an EBITDA margin of 10%, which is lower than the EBITDA margin reported by most competitors. With this figure, I obtained 2032 EBITDA of $7.5-$8.5 billion.

Source: Ycharts

If we also assume an EBIT margin of 8.5%, conservative D&A, capex, and changes in working capital, 2032 FCF would stand at $5.75 million:

My Figures

With the previous financial figures, I would expect significant optimism about Prosus. The cost of equity would most likely decline, so the WACC would be lower than that in the previous case scenario. My results include an implied market capitalization of $470-$475 billion, and an implied share price of $30:

My Results

Risks From New Data Regulations And Lack Of New Opportunities

Prosus invests mostly in online platforms, which may suffer considerable damage from new data regulations. As a result, the company may have to use more resources to protect the data of employees and clients. In this case scenario, I would expect a significant decline in the company’s FCF margins:

Most of our businesses are subject to extensive laws and regulations: legal or regulatory developments, including changes in tax laws, may have an adverse impact on our businesses. A number of new laws and regulations around consumer protection and privacy have been passed globally. Source: Annual Report

In the past, management found investment opportunities at beneficial EV/FCF multiples. The future may not be that sweet. If the company does not identify attractive opportunities for whatever reason, the IRR would most likely decline. As a result, traders may sell shares, which may lead to an increase in the cost of equity and the WACC. In sum, we may see a significant decline in the company’s valuation:

We may not find investment opportunities that fit our strategy and deliver an expected return more than our cost of capital. Portfolio risk may prove to be higher than we assumed to accept, which could negatively impact IRR and lead to a decline in the valuation of Prosus and/or Naspers. Source: Annual Report

Another clear risk comes from miscalculations of the valuation. If management pays too much for its acquired companies, accountants may have to impair the goodwill accumulated. In this detrimental case scenario, we may see a reduction in the book value per share and the expected FCF.

Conclusion

Prosus has a considerable amount of cash to invest in new targets. That’s not all. In my view, if management continues to invest heavily in machine learning and AI technology, more users will visit the company’s classifieds domains. I would also expect significant revenue growth from the offerings proposed by the food delivery business segment. Finally, if management also decides to merge some of its targets, FCF margins would also increase. Under the best conditions, I obtained a target price of $155. Traders are buying shares at less than $30, so I will be a buyer too.

/cloudfront-us-east-1.images.arcpublishing.com/gray/MZZ6VZA235A7XOAVDRAO3AOUWQ.jpg "Vermont regarded forerunner in synthetic intelligence oversight")