Is DXC Know-how (NYSE:DXC) A Dangerous Investment?

A Dangerous Investment?")

Table of Contents

Warren Buffett famously explained, ‘Volatility is considerably from synonymous with danger.’ It’s only natural to take into consideration a company’s stability sheet when you study how risky it is, considering the fact that personal debt is generally involved when a enterprise collapses. We notice that DXC Technologies Organization (NYSE:DXC) does have debt on its equilibrium sheet. But the much more vital query is: how a lot risk is that credit card debt creating?

When Is Credit card debt A Difficulty?

Credit card debt and other liabilities develop into dangerous for a organization when it cannot conveniently satisfy these obligations, either with totally free money stream or by boosting cash at an eye-catching price tag. Section and parcel of capitalism is the system of ‘creative destruction’ wherever failed firms are mercilessly liquidated by their bankers. Nevertheless, a far more frequent (but even now expensive) incidence is where by a firm must concern shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of financial debt is that it generally signifies low cost funds, primarily when it replaces dilution in a organization with the potential to reinvest at high costs of return. When we study credit card debt degrees, we to start with take into consideration equally hard cash and credit card debt degrees, collectively.

Examine out our newest examination for DXC Technologies

What Is DXC Technology’s Net Credit card debt?

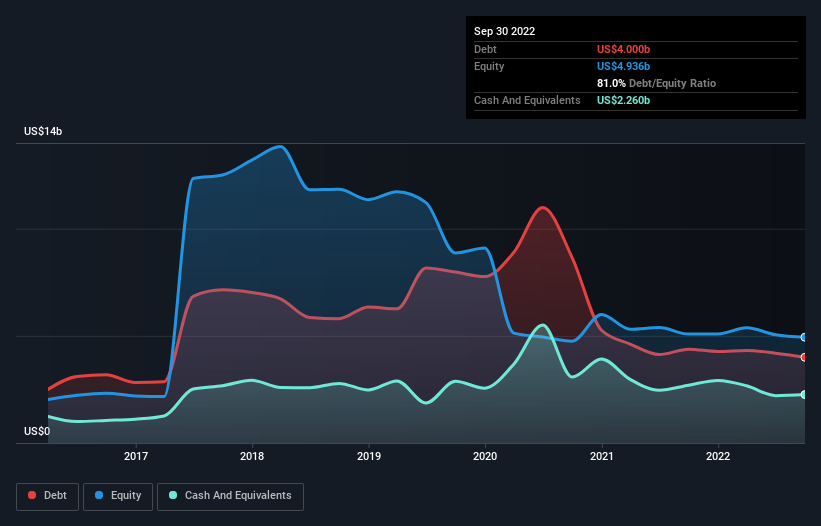

You can click the graphic under for the historical figures, but it reveals that DXC Technological know-how experienced US$4.00b of financial debt in September 2022, down from US$4.38b, a single calendar year right before. Even so, it also experienced US$2.26b in income, and so its net personal debt is US$1.74b.

How Potent Is DXC Technology’s Harmony Sheet?

We can see from the most current harmony sheet that DXC Technologies had liabilities of US$5.87b falling owing within a calendar year, and liabilities of US$6.94b due past that. On the other hand, it had dollars of US$2.26b and US$3.47b well worth of receivables due in a calendar year. So its liabilities outweigh the sum of its cash and (around-phrase) receivables by US$7.07b.

When you look at that this deficiency exceeds the company’s US$6.50b market place capitalization, you could properly be inclined to assessment the balance sheet intently. In the state of affairs where by the company experienced to clear up its equilibrium sheet swiftly, it would seem probably shareholders would undergo in depth dilution.

We use two major ratios to notify us about debt amounts relative to earnings. The 1st is web debt divided by earnings just before curiosity, tax, depreciation, and amortization (EBITDA), when the next is how quite a few instances its earnings just before fascination and tax (EBIT) covers its curiosity price (or its desire address, for brief). The advantage of this tactic is that we get into account both the complete quantum of personal debt (with internet credit card debt to EBITDA) and the precise interest charges related with that debt (with its interest include ratio).

DXC Engineering has a low web financial debt to EBITDA ratio of only .61. And its EBIT addresses its curiosity expenditure a whopping 16.6 moments around. So you could argue it is no much more threatened by its financial debt than an elephant is by a mouse. Better however, DXC Technologies grew its EBIT by 484% very last yr, which is an impressive improvement. That improve will make it even a lot easier to fork out down financial debt heading forward. There is certainly no doubt that we find out most about debt from the equilibrium sheet. But it is upcoming earnings, much more than nearly anything, that will determine DXC Technology’s capacity to retain a healthy stability sheet heading forward. So if you want to see what the specialists consider, you might obtain this free of charge report on analyst earnings forecasts to be intriguing.

Lastly, a business enterprise requires free cash stream to pay back off debt accounting income just never lower it. So we normally check out how substantially of that EBIT is translated into cost-free money circulation. Looking at the most current three years, DXC Know-how recorded free cash flow of 45% of its EBIT, which is weaker than we would anticipate. That weak cash conversion would make it far more complicated to take care of indebtedness.

Our See

Each DXC Technology’s capacity to to include its fascination expense with its EBIT and its EBIT advancement amount gave us comfort that it can cope with its credit card debt. But real truth be instructed its amount of whole liabilities experienced us nibbling our nails. When we consider all the elements pointed out over, it seems to us that DXC Technologies is handling its personal debt really nicely. Acquiring reported that, the load is sufficiently heavy that we would recommend any shareholders continue to keep a close eye on it. When analysing financial debt ranges, the harmony sheet is the obvious location to start. But in the long run, every company can comprise challenges that exist outdoors of the equilibrium sheet. Situation in position: We have spotted 1 warning indicator for DXC Technology you really should be conscious of.

When all is said and done, sometimes its simpler to focus on companies that do not even have to have credit card debt. Readers can entry a listing of progress stocks with zero web debt 100% cost-free, suitable now.

Valuation is advanced, but we are helping make it uncomplicated.

Obtain out no matter if DXC Technology is perhaps over or undervalued by checking out our in depth assessment, which contains good value estimates, threats and warnings, dividends, insider transactions and fiscal well being.

Check out the Cost-free Assessment

Have feed-back on this posting? Involved about the content? Get in contact with us straight. Alternatively, e-mail editorial-group (at) simplywallst.com.

This article by Only Wall St is typical in nature. We deliver commentary primarily based on historical info and analyst forecasts only making use of an unbiased methodology and our articles are not supposed to be economic guidance. It does not represent a advice to get or provide any stock, and does not just take account of your targets, or your money predicament. We aim to carry you extensive-expression concentrated assessment pushed by basic information. Note that our assessment may not aspect in the hottest rate-sensitive company announcements or qualitative materials. Simply Wall St has no position in any stocks talked about.