Enhanced use of client cellular units in-shop drives technological know-how

Shops across segments are accelerating technological know-how deployment options to improve the shopper knowledge and push operational efficiencies, but there are significant variances in between planned know-how rollouts in the grocery/standard items and specialty/division Keep segments, in accordance to the 2022 Related Retail Experience Research by Incisiv, sponsored by Verizon.

“As much more cellular and IoT technology is deployed in retailers, it will travel the will need for much more sturdy network connectivity,” stated Jerri Traflet, managing lover, International Options at Verizon. “It is not surprising that the biggest expected boost in in-retail outlet engineering — client units — is the No. 1 driver for stores to take into consideration adopting 5G deployments.”

The analyze highlights the stress that keep networks will be beneath as respondents have indicated that client cellular product utilization, the amount of engineering purposes and share of know-how that will be deployed in the cloud will all raise considerably in the future 12-24 months. This, combined with the actuality that considerably less than just one-3rd of merchants are at the moment contented with their application reaction time and their potential to deal with community website traffic, reveals a crystal clear disconnect when it comes to in-store systems.

Vital results of the examine include:

- Only 22% of Grocery/Normal Products merchants are glad with their electronic shop practical experience vs. 55% of Specialty/Department retailer shops

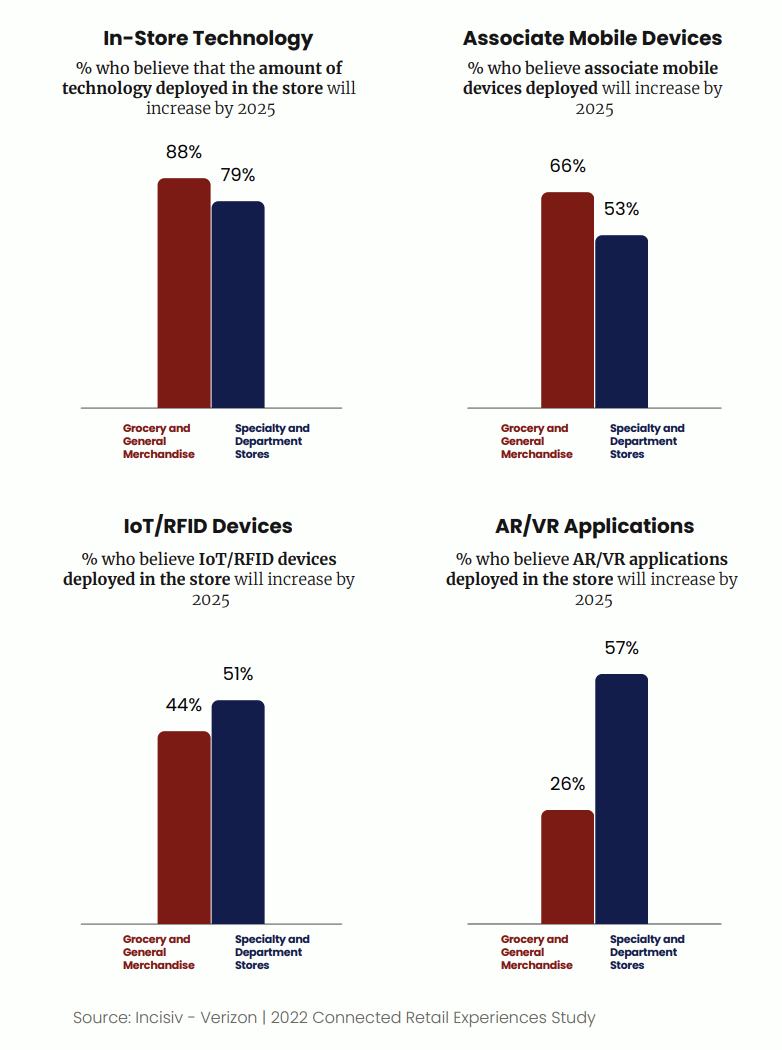

- 93% of suppliers be expecting an enhance in the use of client mobile equipment in shops by 2025 and 83% of merchants foresee an greater sum of engineering deployed in suppliers

- The percentage of associate duties that are automated is expected to triple by 2025 (19% to 62%) for Grocery/Basic Merchandise vendors, a significantly bigger percentage maximize than for Specialty/Section keep vendors, which is predicted to double (37% to 72%)

- Only 20% of Grocery/General Merchandise stores are pleased with their means to take care of peak community visitors vs. 32% for Specialty/Section store retailers

- The No. 1 driver of planned 5G adoption in retailers is the enhance of client mobile equipment in merchants, adopted by the increase in associate cellular units

- Associate effectiveness abilities these types of as authentic-time stock monitoring and affiliate Wi-Fi rated as the optimum priority deployments in the upcoming two decades

Even though stores are content with their overall store knowledge and operations, they are dissatisfied with their store’s electronic maturity, according to the research. “There is a disconnect concerning how shops evaluate their all round retail outlet encounter and their electronic retail store practical experience,” states the report. “While they are content with their total retailer experience and operational effectiveness, they never feel their electronic expertise fulfills shopper expectations. Over the final 18 months, we have seen a quick acceleration in shoppers’ digital adoption and, therefore, a immediate electronic transformation for shops. We have found the retail outlet working experience come to be extra contactless, shopper-associate engagement has become electronic and the store’s purpose has advanced to become a hub of omnichannel fulfillment. The store’s digital fabric (engagement and functions) requirements strengthening due to the fact it will be the critical determinant of long run effectiveness.”

Between retailers:

• 62% are contented with their total retailer encounter

• 66% are satisfied with their store’s operational performance

• 39% are contented with their store’s digital encounter

• 47% are pleased with the success of their keep associates

Over-all, Grocery & Common Goods suppliers are less satisfied with their retail outlet efficiency than Specialty & Division Merchants. The smallest gap amongst formats is in retailer operational effectiveness (62% for grocery vs. 70% for specialty). The greatest hole is their pleasure with the store’s electronic practical experience (22% for grocery vs. 55% for specialty). The report notes that the sample’s bigger proportion of grocery suppliers is driving these gaps. “The elaborate operational issues confronted by grocers all through the pandemic and their slower electronic adoption are the key good reasons for these gaps in fulfillment,” suggests the report.

“While it is good to see suppliers actually searching at how technologies can assistance them increase consumer activities, operational efficiency, and affiliate efficiency, they aren’t as very clear on the community necessities to implement these technologies,” explained Gaurav Pant, chief insights officer, Incisiv. “We observed that priorities are distinctive for Grocery/Standard Products vendors vs. Specialty/Department Shop retailers, but the have to have for a sturdy community won’t change.”